Lifestyle

5 Estate Planning Documents Every Adult Should Have by 50

By Erica Coleman · July 6, 2026

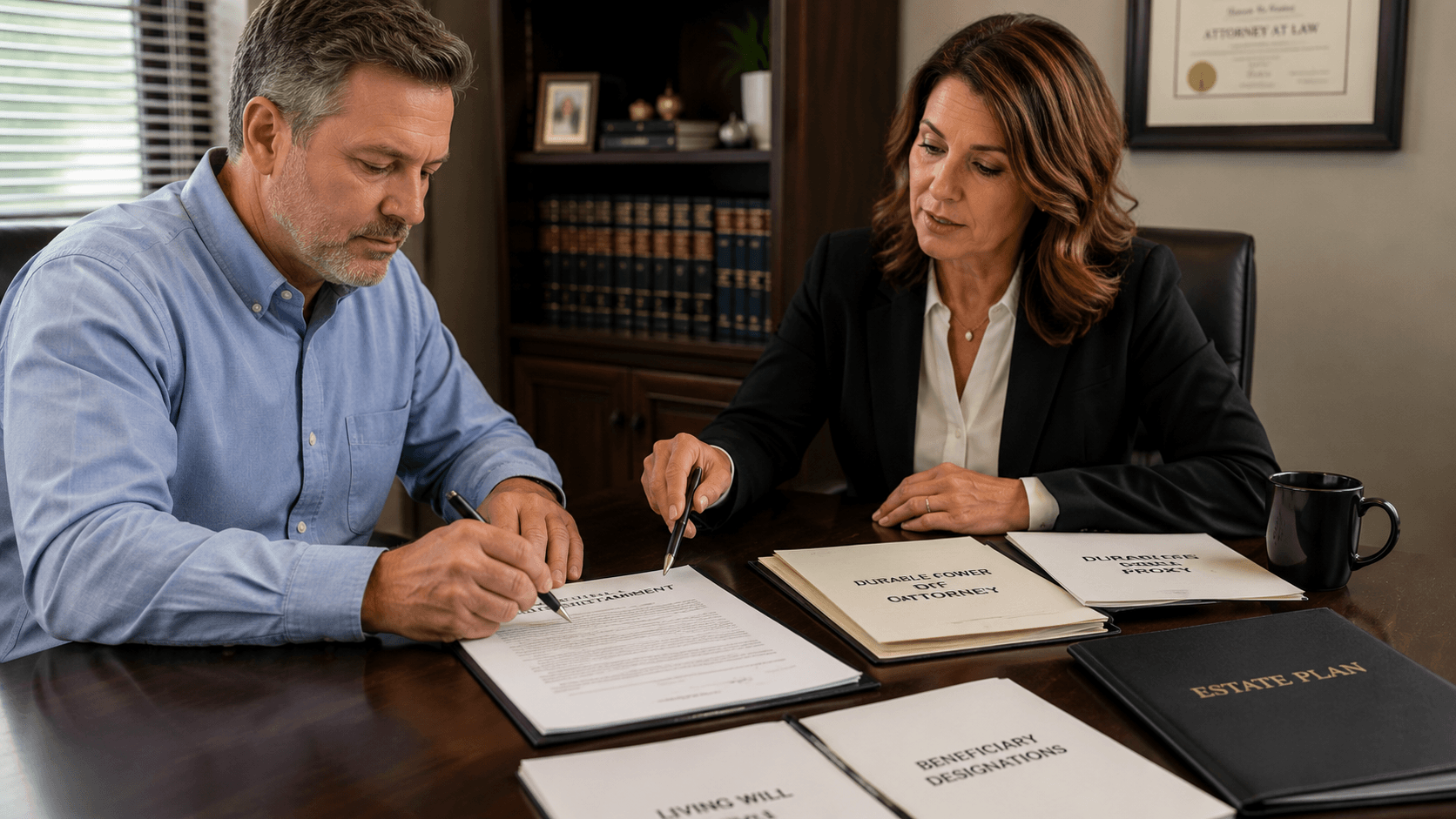

Estate planning is not for wealthy people. It is for anyone who owns property, has children, holds bank accounts, or cares about what happens to their family when they can no longer make decisions for themselves. Here are five documents that every adult should have in place by 50 — and that most do not.

1. A will

A will specifies who receives your assets, who becomes guardian of your minor children, and who serves as the executor of your estate. Without one, the state decides all three — according to a formula that may not match your wishes. Approximately 67% of Americans do not have a will. Creating one through an estate attorney costs $300 to $1,000 depending on complexity. Online legal services offer basic wills for $100 to $200.

2. A healthcare proxy (healthcare power of attorney)

This document names the person authorized to make medical decisions on your behalf if you are unable to make them yourself — after surgery, during a medical crisis, or if cognitive decline removes your capacity. Without a healthcare proxy, your family must petition a court for guardianship to make decisions for you. That process takes weeks, costs thousands, and happens during a medical emergency.

3. An advance directive (living will)

This specifies your wishes for end-of-life medical treatment — whether you want resuscitation, mechanical ventilation, feeding tubes, and other interventions if you are terminally ill or permanently unconscious. Without one, your family members may disagree about what you would have wanted — and the disagreement can fracture families permanently. An advance directive removes the guesswork and the guilt.

4. A financial power of attorney

This authorizes a specific person to manage your finances if you become incapacitated — paying bills, managing investments, filing taxes, accessing bank accounts. Without it, even your spouse may be unable to access accounts held solely in your name. Like the healthcare proxy, this document must be created while you are cognitively competent. Once incapacity is diagnosed, it is too late to execute one.

5. Beneficiary designations — reviewed and current

Life insurance policies, retirement accounts, bank accounts with payable-on-death designations, and investment accounts all pass directly to the named beneficiary — outside of your will and outside of probate. If those designations are outdated — still naming an ex-spouse, a deceased parent, or “my estate” — the assets will go to the wrong person or trigger unnecessary tax consequences. Review every beneficiary designation after every major life event.

These five documents cost a fraction of what their absence costs. An afternoon with an estate attorney — or a focused session with an online legal platform — can complete all five. The cost of not having them is measured in court fees, family conflict, and outcomes you never intended.